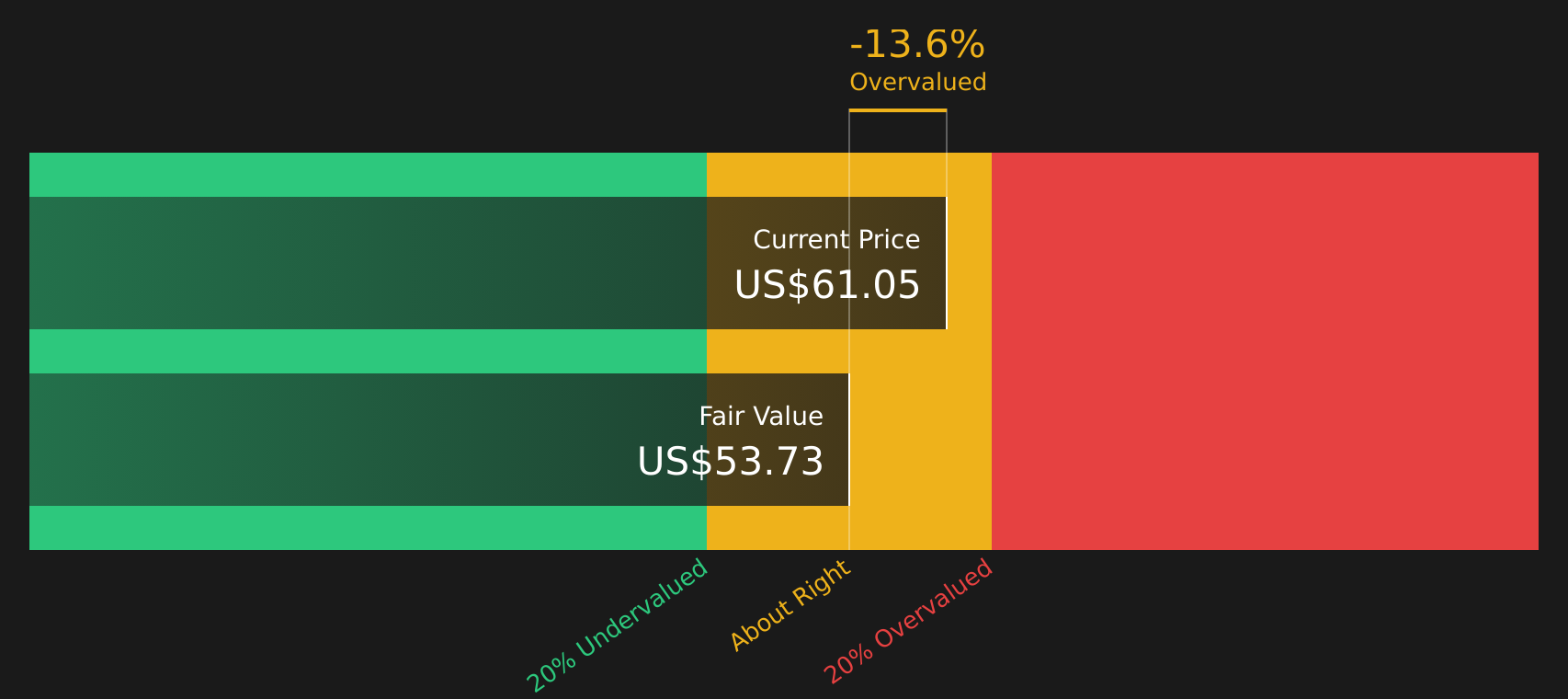

- If you are wondering if the US$61.05 elf Beauty is a cheap price or already bought with high hopes, this breakdown will help you clearly frame that question.

- The share price has recently been under pressure, decreased by 15.8% in 7 days, 33.7% decreased in 30 days, and 21.5% year to date, compared to a decrease of 5.8% last year and a decrease of 25.9% over 3 years.

- The moves come as investors continue to evaluate the broader beauty and personal care sector, with sentiment about the stock’s growth and consumer names changing at different times. For elf Beauty, these changing perspectives create the background for whatever values you see on screen.

- Currently, Simply Wall St’s rating for elf Beauty stands at 2 out of 6. This indicates that the company views some checks as less important but not others. The remainder of this article will unpack those valuation patterns before concluding with a broader consideration of what the market is pricing in.

Elf Beauty scores just 2/6 in our quality reviews. See what other red flags we found in the full quality review.

Method 1: elf Beauty’s Discounted Cash Flow (DCF) Analysis.

The Discounted Cash Flow, or DCF, model takes expected future cash flows and discounts them to today to estimate what the entire business might be worth now. It is essentially asking whether the future income generated for the shareholders is worth in today’s dollars.

For elf Beauty, the Simply Wall St model uses a 2 Stage Free Flow to Equity approach based on cash flow projections. The most recent twelve-month free cash flow is $226.6 million. Analysts’ outlook extends over several years, and the model shows free cash flow of $182 million per year through March 31, 2028. Any estimates beyond that are simply passed on by Wall St rather than based on the analyst’s new estimates.

Pulling the cash flows together, the DCF model comes to an estimated intrinsic value of $53.73 in total. Compared to the recent share price of about $61.05, which means that elf Beauty screens is about 13.6% in this trend.

The result: EXTREMELY PERFECT

Our Discounted Cash Flow (DCF) analysis suggests that elf Beauty’s value could be as high as 13.6%. Find 62 high-quality stocks or create your own search engine to find high-quality opportunities.

Go to the Valuation section of our Company Report for more information on how we arrive at The Fair Value for Elf Beauty.

Method 2: Elf Beauty Price vs Rewards

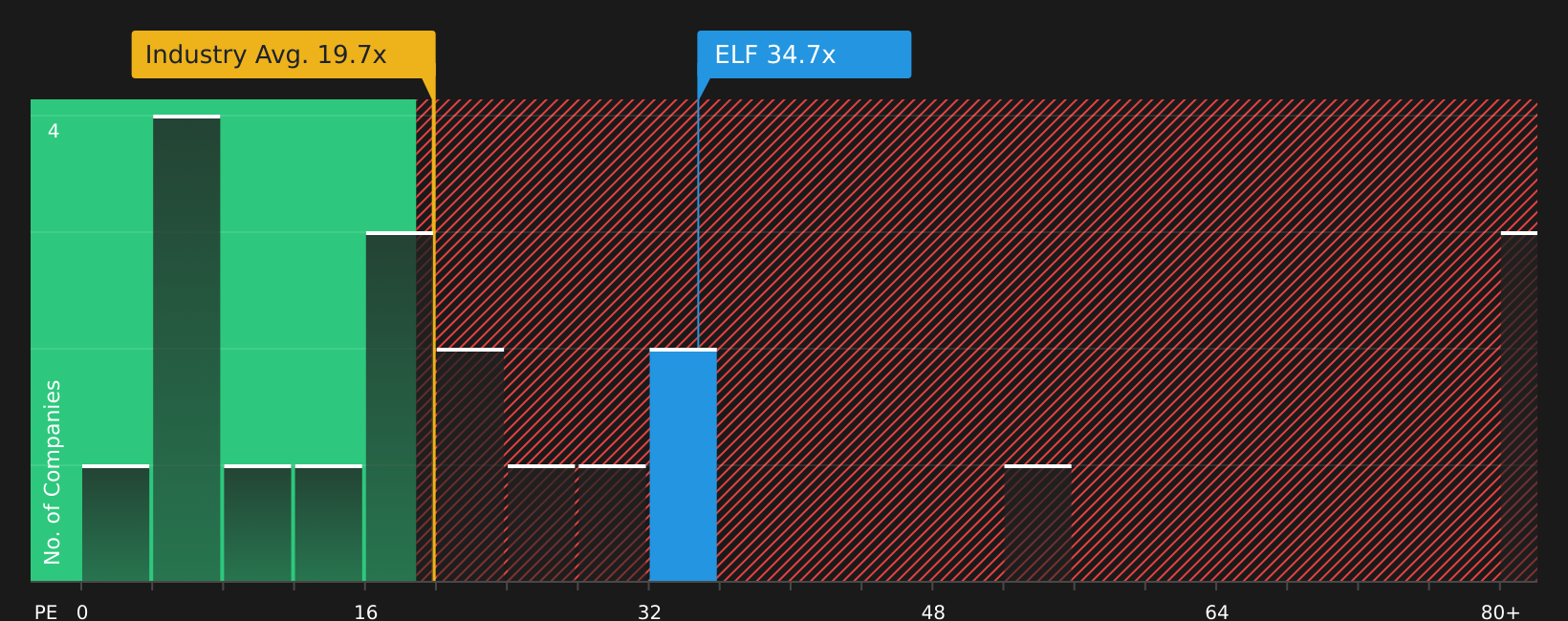

P/E is an important starting point for a profitable company like elf Beauty because it directly correlates what you pay to the earnings the business is already generating. A high P/E usually indicates high market expectations for future growth or low perceived risk, while a low P/E may indicate expectations for moderate growth or high volatility.

Currently, elf Beauty trades at a P/E of approximately 34.7x. That sits above the Personal Products industry average P/E of about 19.7x and above the peer group average of about 10.1x. Simply Wall St also calculates the owner’s “Fair Ratio” P/E, which for elf Beauty is 40.7x. This ratio represents the P/E that can be expected based on factors such as earnings growth, profit margins, industry, market capitalization and company-specific risks.

Compared to a simple industry or peer comparison, the Fair Ratio aims to adapt to the company’s situation, rather than assuming that all peers deserve the same frequency. Since elf Beauty’s current P/E of 34.7x is below its Fair Ratio of 40.7x, this trend suggests that the shares appear undervalued on multiple earnings.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not managers. Discover our top 20 founder-led companies.

Improve Your Decision Making: Choose your own Elf Beauty story

Earlier it was said that there is a better way to understand the quality of the value. Reports take center stage as an easy way for you to explain your story for elf Beauty, connect that story with clear assumptions for future revenue, earnings, signals and fair value, then compare that fair value to the current share price to decide if the stock looks rich or cheap based on your circumstances.

On Simply Wall St’s Community page, Reports are available as an accessible tool used by millions of investors. Each report includes a clear explanation of what you think will lead the business to a forecast and accurate value that automatically updates as new information such as earnings, guidance or news arrives.

For elf Beauty, one investor Narrative currently supports a fair value of US$152.71 with a projected revenue growth of 30.8%, a dividend yield of 10.0%, a discount rate of 8.0% and a forward P/E of 25.0x. A more conservative narrative has a fair value of US$85.00 with revenue growth of 12.815783%, dividend yield of 14.305136%, discount rate of 7.429326 and forward P/E of 22.956265x. Your job is to decide which story, if any, best fits your vision of the company.

Do you think there is more to the story of elf Beauty? Go to our Community to see what others are saying!

This Simply Wall St article is general in nature. We provide opinions based on historical data and analyst estimates using an unbiased approach and our articles are not intended as financial advice. It does not make an offer to buy or sell any property, and does not consider your motives, or your financial situation. We are committed to bringing you long-term analysis focused on fundamentals. Note that our review may not cover recent releases that are not sensitive to pricing or quality materials. Simply Wall St has no position in the stocks mentioned.

New: Manage all your stock portfolios in one place

We made the ultimate portfolio partner for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Alerting of New Warning Signs or Hazards by email or phone

• Track the Quality of your goods

Try Demo Portfolio for free

Have a comment about this article? Are you concerned about the news? Contact us directly. Alternatively, email editorial-team@simplywallst.com

#Time #Reassess #elf #ELF #Sharp #Share #Price #Pullback