Current share performance and trade balance

With no single headline attracting attention, Elf Beauty (ELF) is drawing investor interest after a period of weak share performance, including a 34% drop in the past month and a 24% drop in the past 3 months.

At its last close of US$61.05, the Oakland-based beauty company has a market value of about US$3.9b. It reported annual revenue of US$1.52b on revenue of US$103.94m.

Check out our latest review for elf Beauty.

The recent decrease of 34% in one month of the monthly price return of 24% has come down in 3 months after a long period during which the 5-year average return has been rising by 126.61%. The recent trend seems to be fading even as the long-term story remains positive.

If the recent pullback has had you exploring the possibilities of brand names, it may also be a good time to expand your search and uncover 20 founder-led companies.

With elf Beauty now trading below recent levels, despite annual revenue of US$1.52b and net income of US$103.94m, does the pullback open a value gap, or is the market already factoring in future growth?

Most Popular Report: 76% No value

According to a closely followed story from WallStreetWontons, the fair value of about $251 for elf Beauty sits well above the last session at $61.05, which shows the latest effect in a very different way for anyone focused on long-term potential rather than short-term price fluctuations.

Elf Beauty has experienced significant growth in recent years, and many key factors have contributed to this success. Here are some of the key factors that drive the company to grow:

Strong Brand Positions and Product Design: elf Beauty has established itself as a leading brand in the mass beauty category, offering high quality products at affordable prices. The company is known for its innovative approach to product development, constantly coming up with new and exciting products that attract more customers.

Read the full story.

I wonder what will happen to the higher quality sound? The report relies on the network’s steady strength, growing reach, and unsustainable profit margins.

Result: A fair price of $251 (UNDERVALUED)

Read the report in detail and understand what drove the forecast.

However, the report could be damaged if the decline in sales growth continues and rising costs continue to pressure margins, especially considering that higher prices are now reflected in the share price.

Find out about the important dangers of this Elf Beauty story.

Another quality lens: multiple rewards send a different message

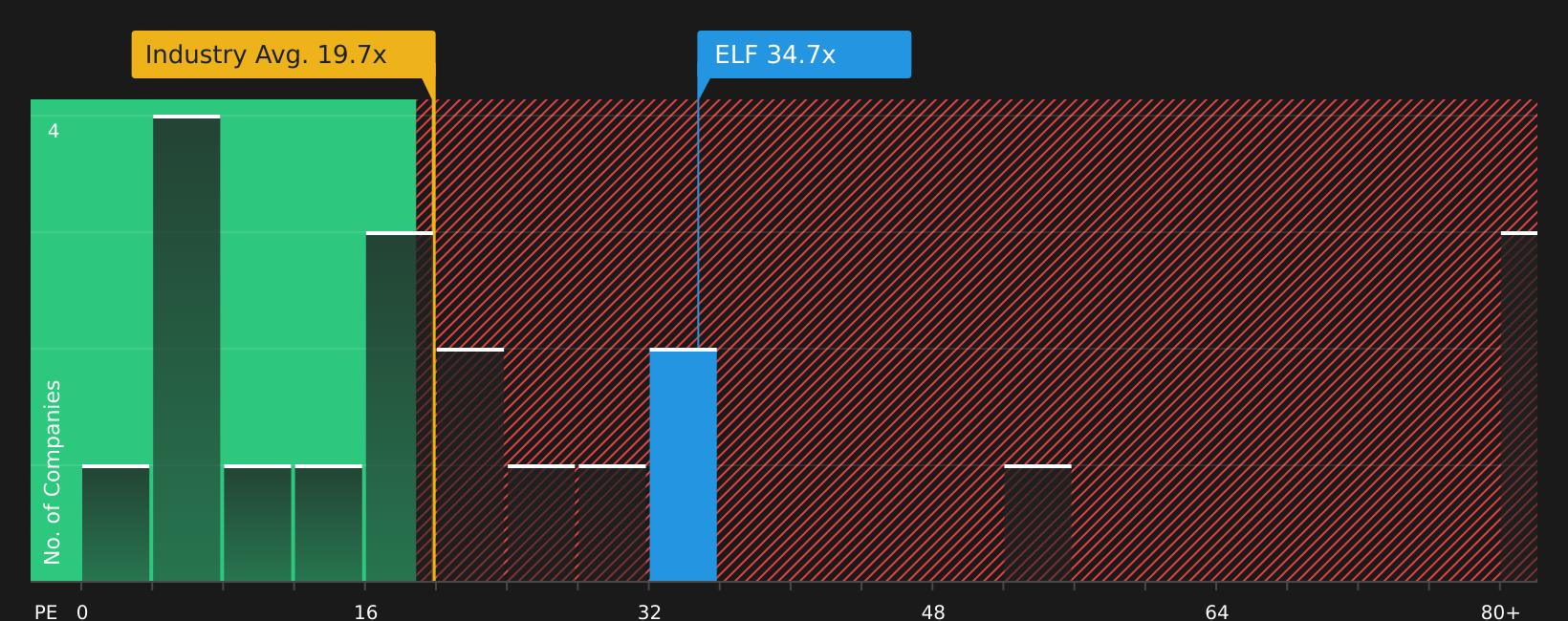

The most popular valuation estimate of $251 is based on strong growth and profit assumptions. In contrast, elf Beauty trades at a P/E of 34.7x, which sits below its fair value of 41.2x but above peers at 10.1x and the broader Personal Products industry at 19.7x. That combination of an apparent discount to fair value and a premium to peers leaves a simple question: is this a value story at a high entry price or just a booming business waiting to be relaunched?

For a closer look at how this P/E gap stacks up against peers and the relevant ratio in practice, See what the numbers say about this price – find out in our value breakdown.

Simply Wall St does a discounted cash flow (DCF) on every stock in the world every day (see elf Beauty for example). We show the whole number in detail. You can track the results in your watchlist or portfolio, and be alerted when this changes, or use our stock checker to find 61 high-quality stocks. If you save the screen we even alert you when new companies are playing – so don’t miss a potential opportunity.

Next Steps

With opinions clearly divided between risks and rewards, this is the moment to look at the data first and move quickly as the debate continues. Start with 3 important rewards and 1 important warning sign.

Ready to hunt for more opportunities?

If elf Beauty is on your radar, don’t stop there. Post similar comments to get other opinions before the market does.

This Simply Wall St article is general in nature. We provide opinions based on historical data and analyst estimates using an unbiased approach and our articles are not intended as financial advice. It does not make an offer to buy or sell any property, and does not consider your motives, or your financial situation. We are committed to bringing you long-term analysis focused on fundamentals. Note that our review may not cover recent releases that are not sensitive to pricing or quality materials. Simply Wall St has no position in the stocks mentioned.

New: Manage all your stock portfolios in one place

We made the ultimate portfolio partner for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Alerting of New Warning Signs or Hazards by email or phone

• Track the Quality of your goods

Try Demo Portfolio for free

Have a comment about this article? Are you concerned about the news? Contact us directly. Alternatively, email editorial-team@simplywallst.com

#Elf #Beauty #ELF #Valuation #Share #Price #Pullback